Testing Form Handler

The Exchange: The Truth About Advisor Contingency Planning (Ep. 27)

Advisor Contingency Planning In the first-ever episode of The SRG Exchange, SRG’s consulting team comes together for a candid discussion on one of the most overlooked and essential components of running a financial advisory firm: contingency planning. Drawing from real client experiences and day-to-day advisory work, the team breaks down what advisors often misunderstand, what regulators actually expect, and what a truly functional continuity plan must include. This conversation sheds light on the operational, legal, and relational challenges that surface when a plan fails, and offers practical steps to help advisors protect clients, revenue, and family long before an emergency occurs. Why Contingency Planning Still Falls Short The episode opens with a direct reality check. While nearly every advisor knows they should have a contingency plan, very few have one that would truly work under pressure. The team discusses common gaps they see across the industry, including: plans that exist only on paper and do not reflect firm reality unclear successor instructions incorrectly structured agreements that fail when tested BD or custodian forms mistaken for full plans They explain why these gaps become critical risks, not just for compliance, but for clients, staff, and family members who are left scrambling. Understanding What a Real Plan Looks Like From valuation considerations to internal decision-making authority, the team outlines the building blocks of a functional, actionable plan. Key insights include: why a contingency plan must tie directly to a firm’s legal entity structure the importance of identifying who actually has the authority to take over why buy-sell agreements are not always enough how entity maintenance impacts continuity readiness the role of service agreements, compensation, and communication plans The takeaway is clear. Effective contingency planning is not one-size-fits-all. It must be tailored to the firm’s ownership structure, internal roles, and growth stage. Lessons From the Field The discussion includes real scenarios pulled from SRG’s consulting work, including both successes and cautionary tales. Advisors will hear: what happens when documentation does not match operational reality how unexpected disability or death can affect valuation and transition options why even well-intentioned plans break down during crisis how firms that plan proactively preserve value and avoid chaos These examples ground the conversation in real-world impact and show exactly how preparation, or lack of it, plays out. Practical Guidance for Advisors The team shares tangible steps advisors can take to strengthen or build their plan, including: conducting a full review of existing agreements validating successor roles and responsibilities documenting operational continuity steps maintaining updated books, records, and entity documents ensuring clients know the firm has a plan in place They also discuss how often plans should be revisited, and why regular maintenance matters just as much as initial creation. Conclusion: Protecting What Matters Most The episode closes with a reminder that contingency planning is not just a compliance requirement. It is a fiduciary responsibility. By proactively addressing these issues, advisors protect their clients, their staff, the value of their firm, and the people they care about. The key takeaway: a contingency plan is not complete until it works in real life, under real pressure. Advisors who invest the time to get this right are better positioned to navigate the unexpected and maintain stability for their business and everyone who depends on it. Who is Featured in This Episode Nicole Frey, CFP® David Grau Jr., MBA Julia Sexton (Sullivan), CVA Ryan Grau, CVA, CBA Kristen Grau, CPA, CVA, CEPA Parker Finot

RIA Leaders: Top 10 firms by number of financial advisors for 2025

By: Tobias SalingerPublishing Date: November 25, 2025 Whether or not publicly traded wealth management firms disclose their headcounts of financial advisors in their quarterly earnings, the number represents a closely watched industry metric. So the below rankings of fee-only registered investment advisory firms with the most advisors in Financial Planning’s annual RIA Leaders study reveal which companies are hiring and training at the largest volume. Executives that have led giant wealth management firms such as Ameriprise, Wells Fargo Advisors, Morgan Stanley and Merrill to remove their quarterly headcount figures frequently argue that the number of advisors is no longer as important as the amount of client assets, organic growth, productivity or, of course, revenue and profit. On the other hand, advisor headcount affects each of those other figures. And the firm with more advisors than any other, LPL Financial, proudly shared the size of its ranks of 32,128 advisors at the end of the third quarter. Fee-only RIAs such as Savant Wealth Management, Moneta Group Investment Advisors and EP Wealth Advisors don’t approach that level of scale. However, they’re operating in a field with a stagnant overall headcount of advisors, a massive succession challenge amid looming retirements and a possible hiring shortfall in the face of growing consumer demand for advice. Technology may solve part of those problems, said David Grau, the CEO of consulting firm Succession Resource Group. He compared the potential of technology like artificial intelligence to the difference between moving a big pile of wood with or without a wheelbarrow. While there’s “obviously a need” to hire more advisors, that dearth of incoming talent isn’t “as bad or as out of proportion as we have made it out to be in the past,” due to the AI and other tech, Grau said. To read the full article, please visit: https://www.financial-planning.com/list/fee-only-rias-with-the-most-financial-advisors-in-2025 Disclaimer This article was first published by Tobias Salinger The original article can be found here. All rights to the original content are held by FinancialPlanning.com.

The RIA founder’s dilemma: Choose your successor or sell

By: Tobias SalingerPublishing Date: November 24, 2025 This is the 28th installment in a Financial Planning series by Chief Correspondent Tobias Salinger on how to build a successful RIA. See the previous stories here, or find them by following Salinger on LinkedIn. Registered investment advisory firm founders who build profitable businesses with a stable base of clients must one day decide how they would like to pick a successor. With around a third of the industry’s financial advisors expecting to retire in the next decade and a looming potential shortfall of professionals compared to the demand for advice, RIA successors will either emerge internally or through an acquisition. One path at that fork in the road likely poses a more lucrative exit from the field, but with less autonomy about the transition of clients to a new advisor after selling the firm. The other trail enshrines an advisor’s legacy with those clients under the same company with hand-picked successors. But developing those successors has proven challenging for many firms that are simultaneously fielding higher bids from RIA aggregators. Internal successions equate to a “natural discount of at least 30%” compared to selling to private equity-backed firms and other RIA and advisory team consolidators, said Steven Tenney, a former advisor who is the founder of consulting and RIA coaching firm Grandview & Co. and the author of a new book published earlier this month called, “RIA Succession Alpha.” They also require “empowering the next generation of successors,” so that “the firm starts to run on its own, with less input from the founder,” he noted. After an RIA has created its plan, its one or more owners and their team must work together through the transition. “Without clarity, you’re aimless, and so you’ve got to start there,” Tenney said. “Many people treat succession planning as an event, as opposed to a necessary part of business. There is near-perfect overlap between succession planning and good business planning. It’s one and the same.” To read the full article, please visit: https://www.financial-planning.com/news/how-to-hire-and-advance-an-ria-successor Disclaimer This article was first published by Tobias Salinger The original article can be found here. All rights to the original content are held by FinancialPlanning.com.

Contingency Planning Resources for Financial Advisors

Plan for the Unexpected Creating a contingency plan is one of the most important — and most overlooked — things you can do as a business owner, especially in a highly regulated industry. We create simple yet effective turnkey solutions for financial services professions (independent RIAs, financial advisors, accountants, and agents) looking to protect their clients, family, and their business by leveraging years of experience, industry-specific form agreements, and strategic planning resources from SRG. Learn more about our Contingency Planning Services Contingency Plans for Financial Professionals 3‑minute read A quick overview of the main types of contingency agreements (buy‑sell, reciprocal, retainer) and when each structure makes the most sense. Read the Overview Death/Disability Considerations – Ep. 21 30-minute listen A candid discussion on what most advisors overlook in their death and disability planning, and how to avoid leaving your clients and family with chaos instead of a clear plan. Listen to the Episode Contingency Planning FAQs for Finical Advisors 5‑minute read Straightforward answers to the questions advisors ask most: partners, valuation, discounts, funding, taxes, and what happens if your chosen partner can’t follow through. View the Top FAQs Protect Your Loved Ones Plan for unforeseen events such as death, disability, and loss of license. Ensure your legacy is passed on to those for whom you have worked so hard. Protect Your Business’ Value Whether you have identified a contingency partner or not, we can help you create a written plan to ensure the business and clients are taken care of and your family receives value should something ever happen.

Building a Lasting Legacy Through Equity Sharing with Brian Cochran

Turning Ownership Into Opportunity For Brian Cochran’s second-generation advisory firm, the path toward long-term success required more than just organic growth; it required intentional career-building for continued legacy and internal succession. After assuming full ownership of the business, the firm’s new leader recognized a critical opportunity: transform equity participation from a future concept into a tangible, motivating force for key team members. Although Brian’s firm already had a robust benefits structure, its principal understood that true retention goes beyond compensation. The next step was to create a deeper sense of belonging and shared purpose. The challenge wasn’t just deciding if to share equity — it was determining how to do it in a way that aligned with his vision for the firm. The owner knew that opening the door to ownership could be transformative, but it also carried risks. The firm wanted to reward and retain high performers without compromising financial stability or creating future complications. Among the key questions they faced: Timing plays a key role in shaping both value and price. A valuation is a recurring tool that helps you plan proactively—identifying opportunities to strengthen your business and enhance value before you need to act. In contrast, price happens once, when your firm, finances, and personal goals are all aligned and ready for transition. Recognizing that the stakes were high, the firm sought expert guidance to design a plan that would balance growth, fairness, and sustainability. The Turning Point: Choosing Succession Resource Group Brian Cochran turned to SRG’s Equity Sharing team, led by Julia Sexton, CVA®, Director of Strategic Organization Planning. The decision to partner with SRG was rooted in one defining principle: expertise matters. What impressed Brian most was SRG’s ability to ask the right questions. Rather than offering prepackaged solutions, SRG invested the time to deeply understand the firm’s structure, team culture, and long-term vision. Each conversation helped Brian’s firm refine its objectives and uncover what truly made his practice unique. The Discovery Process: Defining the Dual Goals As the project unfolded, SRG helped Brian Cochran articulate two distinct yet complementary goals: The Strategy Through deep discussion and scenario modeling, SRG helped Brian’s firm recognize that these objectives could be met through a two-part strategy. This flexible dual-plan design enabled Brian’s firm to reward both tenure and potential, ensuring that no key contributor was left out of the long-term vision. The Solution: Designing a Balanced and Sustainable Plan Led by Julia Sexton, CVA®, Director of Strategic Organization Planning, SRG developed a personalized plan that aligned with the firm’s culture and goals. The resulting Equity Sharing Plan provided a balanced framework that: Key Features of the Plan Implementation: A Seamless Process with Expert Guidance One of Brian’s early concerns was how complex and intimidating the process might be. SRG’s structured, hands-on approach quickly alleviated those fears. SRG coordinated directly with the firm’s tax advisor, ensuring alignment at every stage. They clearly explained each option, its implications, and its benefits, translating technical and legal details into actionable insights. From a legal and administrative perspective, SRG’s diligence and communication created peace of mind. Nothing fell through the cracks, and every step built confidence in the final outcome. The Rollout: Bringing the Team On Board Once the plan was finalized, the firm turned its attention to rollout and communication, a critical step in ensuring understanding and enthusiasm with the team. SRG equipped Brian Cochran with the necessary tools, talking points, and documentation to facilitate one-on-one conversations with eligible team members. These personalized discussions helped participants understand: The Client’s Reflection: Confidence in the Future Reflecting on the process, Brian Cochran expressed deep satisfaction with the results and gratitude for SRG’s partnership. The success of the plan reinforced a broader insight: succession and equity planning aren’t just about ownership, they’re about creating a culture of shared success. The Takeaway: Partnership That Builds the Future This case exemplifies SRG’s mission to help advisors, RIAs, and other financial firms align their people, purpose, and planning for enduring success. Through the thoughtful leadership of Julia Sexton CVA®, Brian Cochran gained not just a plan but a strategic framework for growth, retention, and value-building initiatives. The Equity Sharing Plan now serves as both a meaningful reward system and career-building roadmap, ensuring that the firm’s brightest talent can build their future within the organization. Download the Case Study Please enable JavaScript in your browser to complete this form.Please enable JavaScript in your browser to complete this form. Name * FirstLast Phone Work Email *How Did You Hear About SRG? *— Select Choice —ConferenceDirect MailExisting/Past ClientGoogle AdWordsOtherReferralSocial MediaSeminar/WorkshopWebinarWebsite Download

The top fee-only RIAs ranked by AUM in 2025

By: Tobias SalingerPublishing Date: November 19, 2025 Read the full article here. The excerpt below is a brief snippet. To read the full article, please click the link above. Eventually, the largest RIA aggregators could begin to see some advisors “splinter off” toward more independence out of companies that have become “a large national or international enterprise,” said David Grau, CEO of consulting firm Succession Resource Group. For now, movement into those firms and out of the wirehouses and other brokerages is feeding into the biggest RIAs, as are two other trends: teaming and companies offering advisors many essential services in one place. “They’re able to compete on price, scale and service level. It’s really hard to compete with them, and, so, if you can’t beat ’em, join ’em,” Grau said. “The aggregation is at a really good inflection point for our industry. We’ve got large enough firms that can now focus on mentoring and training the next generation, not buying a book.” Over the past decade, RIAs have expanded at an 11% compound annual growth rate due to asset appreciation and advisors’ gravitation toward them, research firm Cerulli Associates found in a study released earlier this month. At the same time, more than two-thirds of RIA executives with billion-dollar firms said organic growth is a strategic priority, and 83% said advisors’ lack of available time to focus on that is constraining their efforts around that goal. Regardless, the firms with at least $5 billion are vacuuming up the RIA channel. In the past five years, their client assets jumped at an average annual rate 21% and their advisor headcounts surged by 19% while their share of the channel’s assets soared by 18 percentage points. Disclaimer This article was first published by Tobias Salinger. All rights to the original content are held by FinancialPlanning.com.

Planning for internal RIA succession? Experts say it takes a decade

By: Tobias SalingerPublishing Date: November 17, 2025 This is the 27th installment in a Financial Planning series by Chief Correspondent Tobias Salinger on how to build a successful RIA. See the previous stories here, or find them by following Salinger on LinkedIn. The growth of registered investment advisory firms is turning their widespread lack of succession plans into an even bigger problem. But planning to exit the business someday is typically much easier said than done for many financial advisors, who operate in a widely dispersed field of tens of thousands of RIAs and usually enjoy working with their clients much more than completing administrative tasks. If they aim to retire in the next decade with an internal succession that doesn’t involve selling the business to an RIA consolidator or another large wealth management firm, they may have already delayed their succession planning too long. “You need to start early. You can’t be wanting to retire in five years and think that you’re going to start this a year before you retire,” said Dominique “Dom” Henderson, a planner who is the founder of Dallas-based RIA firm DJH Capital Management and the Jumpstart Coaching Lab, an advisor training and coaching firm. He recalled a presentation at an industry conference this year by an advisor whose firm has about $300 million or $400 million in client assets but two failed succession plans in the past. “She had been trying at this for 15 years, so this is the reason that people hire consultants to help them with this,” Henderson added. “It’s a lot of moving pieces, so my advice to anyone is, start early.” To read the full article, please visit: https://www.financial-planning.com/news/how-rias-can-create-a-succession-plan Disclaimer This article was first published by Tobias Salinger The original article can be found here. All rights to the original content are held by FinancialPlanning.com.

Equity Compensation: A Technical Comparison between Restricted Equity Grants

Please enable JavaScript in your browser to complete this form.Please enable JavaScript in your browser to complete this form. Name * FirstLast Phone Work Email *How Did You Hear About SRG? *— Select Choice —ConferenceDirect MailExisting/Past ClientGoogle AdWordsOtherReferralSocial MediaSeminar/WorkshopWebinarWebsite Download Empower your team and strengthen the long-term health of your business with SRG’s “Equity Compensation: A Technical Comparison Between Restricted Equity Grants” white paper. This practical, easy-to-understand resource breaks down the key differences between Restricted Stock Awards (RSAs) and Restricted Stock Units (RSUs) — two of the most common tools for sharing ownership value and aligning employees with your company’s future. Whether you’re designing a new equity plan, preparing for growth, or looking to retain top talent, this guide clarifies the structural, tax, and ownership considerations every business owner should understand. From grant mechanics and vesting to 83(b) elections and S-Corp compatibility, you’ll learn how each approach impacts control, complexity, and long-term planning. Explore how the right equity strategy can motivate your team, support succession goals, and protect the value you’ve built. Download the white paper today and make confident, informed decisions about equity compensation.

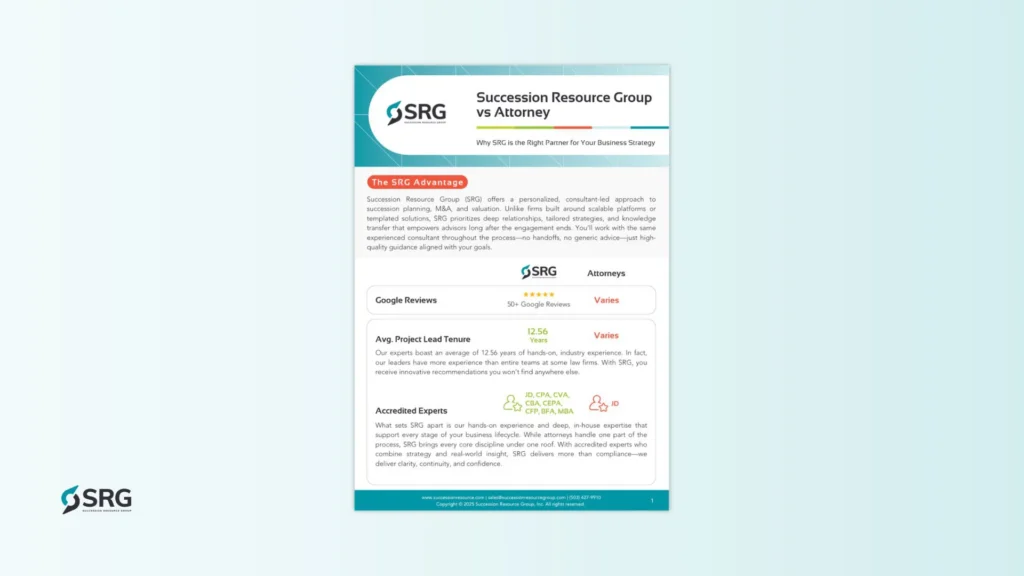

Attorney vs Succession Resource Group

Think Your Attorney Can Handle It? Think Again. Many advisors believe their attorney can “handle it”, but that’s where critical gaps emerge. Attorneys focus on contracts and compliance, but they’re not built to optimize your entity structure, tax strategy, valuation, growth plan, or exit strategy, and they usually have no experience with the financial services industry. SRG brings everything under one roof — so you don’t have to coordinate a dozen different specialists on your own. We handle the moving parts, align every advisor, and keep your plan strategic and focused. Attorneys can check the legal box; SRG delivers the complete, future-ready blueprint your business and clients deserve. Please enable JavaScript in your browser to complete this form.Please enable JavaScript in your browser to complete this form. Name * FirstLast Phone Work Email *How Did You Hear About SRG? *— Select Choice —ConferenceDirect MailExisting/Past ClientGoogle AdWordsOtherReferralSocial MediaSeminar/WorkshopWebinarWebsite Download